On April 24, Ebang International officially filed for an initial public offering (IPO) with the U.S. Securities and Exchange Commission (SEC). The company plans to list on either the New York Stock Exchange (NYSE) or NASDAQ, aiming to raise up to $100 million.

This marks Ebang International’s third attempt to go public. Its two previous bids to list on the Hong Kong Stock Exchange failed, reportedly due to non-compliance with the “listing suitability principle” and a series of ongoing lawsuits.

The timing of this latest effort is far from ideal. It comes amid allegations of financial fraud against its rival Canaan Creative by short-seller firms, as well as a broader crisis of confidence facing Chinese companies listed in the U.S. (ADRs). Given these headwinds, Ebang’s pursuit of a U.S. listing remains highly uncertain.

So why is Ebang pushing ahead now?

Launching an IPO under such adverse conditions could hardly be worse. Yet Ebang’s determination stems from a pressing financial need: the company is critically short of cash.

According to its prospectus, Ebang International reported revenues of $319 million in 2018 and $109 million in 2019, with net losses of $11.81 million and $41.07 million, respectively. In 2019, its revenue was only half that of its peer, Canaan Creative.

The company’s cash flow is also under severe strain. Its net cash flow from operating activities was -$108 million in 2018 and -$13 million in 2019. As of December 31, 2019, Ebang had $13.74 million in other payables and $11.83 million in accounts payable.

Historically, Ebang has relied on operating cash flow, shareholder contributions, and bank loans to fund its working capital. However, with profitability declining and cash flow tightening, its existing resources are insufficient to support its growth plans.

Interchain Pulse notes that Canaan Creative has not released a new mining hardware product in nearly a year—its latest Avalon E12 series launched last May.

Meanwhile, competitors like Bitmain, MicroBT, and Canaan have all recently launched high-performance miners with significantly improved power efficiency: Bitmain’s 7nm Antminer S19 series, MicroBT’s 8nm Whatsminer M30S, and Canaan’s Avalon A11 series.

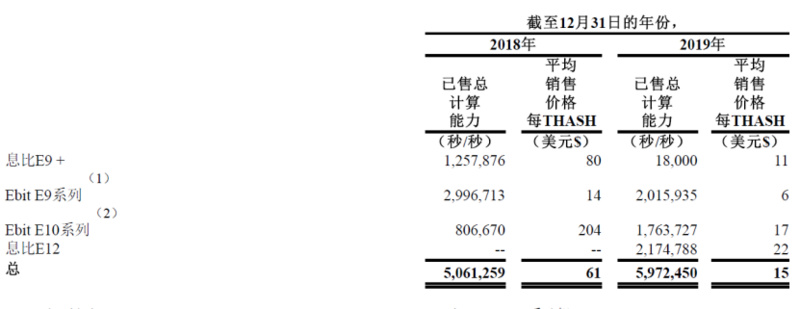

Ebang’s Avalon E12 series remains a 10nm miner, delivering 55 TH/s at 57 W/TH—performance roughly on par with Canaan’s previous-generation Avalon A1066 Pro.

Although Ebang states in its prospectus that it completed the design of its latest 8nm and 7nm chip-based miners in 2019, these products have yet to hit the market.

This delay is likely linked to a sharp drop in R&D spending. Ebang’s R&D expenses fell 69.2% year-over-year to $13.4 million in 2019, down from $43.5 million in 2018. Reduced investment has left its hardware lagging behind competitors, undermining its price competitiveness.

Financial data shows that in 2019, Ebang’s mining hardware sold for an average of $15 per terahash (TH), compared to $19 per TH for Canaan’s equipment.

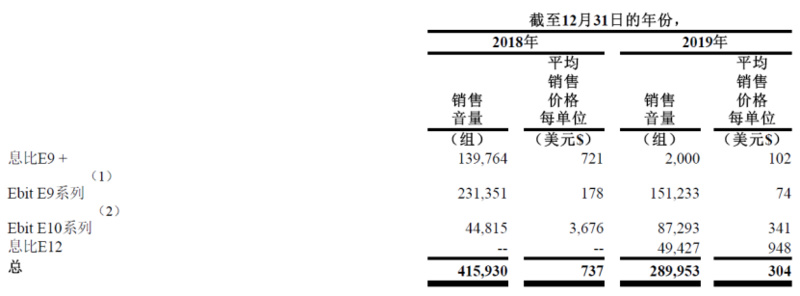

Sales volume has also plummeted. Ebang sold approximately 416,000 units in 2018, but only 290,000 in 2019. Over the same period, the average selling price per unit dropped from $737 to $304.

Faced with a steep decline in its core business, Ebang is seeking new growth avenues. Unlike Bitmain and Canaan, which have invested in AI, Ebang is turning to the potentially faster-revenue-generating cryptocurrency exchange business.

Its prospectus outlines plans to establish a cryptocurrency exchange outside China, offering trading services to the crypto community.

However, given the regulatory uncertainty surrounding crypto exchanges in both the U.S. and China, this pivot represents a high-risk strategy that adds further uncertainty to Ebang’s IPO prospects.

U.S. Listing Bid Hangs by a Thread

Beyond its exchange ambitions, an even greater source of uncertainty for Ebang’s U.S. listing is its unresolved legal history.

For instance, in September 2018, Ebang became entangled in the collapse of the “Yindouwang” P2P platform. An unexplained transfer of RMB 520 million between Ebang and Yindouwang’s controller led some victims to allege asset diversion.

Also in 2018, miner customer Ma Xiaoyun sued Ebang after purchasing 500 Avalon E10 miners for RMB 13 million. The units experienced frequent failures, requiring 873 repair visits within three months. That lawsuit remains unresolved.

Last December, A-share listed company Zhongying Interconnection announced that its subsidiary had paid Yibang International for mining equipment but never received it, alleging contract fraud. Yibang International countered by accusing Zhongying of malicious reporting and filed a lawsuit. The legal dispute between the two remains unresolved.

Beyond this litigation, Yibang International's current push for a U.S. listing faces another major hurdle: the wave of trust crises ignited by Luckin Coffee.

Since Luckin admitted to financial fraud on April 2, short-sellers have targeted other U.S.-listed Chinese firms like Genshuixue (GSX) and iQiyi with accounting fraud allegations. Yibang's competitor, Canaan Creative, which went public last November, has seen its performance plummet—reporting a massive loss and a 70% drop in market cap—and has also faced fraud accusations from short-sellers.

This series of trust crises has further clouded Yibang International's U.S. listing prospects. However, if it fails to tap into the capital markets, the company risks its very survival amid intensifying competition from other mining hardware manufacturers.