It is now a consensus among investors and industry participants that the crypto market is in a bear phase. However, winter is precisely the time to prepare for spring. What grows in the future depends on what is sown today. Huobi Research interviewed more than 20 globally prominent investment institutions, using their current status, investment philosophies, and strategic focuses as case studies. Our goal is to understand how these institutions view the industry's present and future, and to identify promising sectors.

Our interviews revealed that most institutions are taking a "watch more, act less" approach. They are prioritizing infrastructure projects, with ZK, new public blockchains, and middleware drawing the most attention. At the application layer, DeFi, gaming, and social projects rank highest. DeFi remains the most favored sector among institutions, while gaming and social are the most debated.

Key institutional focus areas and their rationale:

● ZK is seen as a potential core driver of the next cycle, with long-term value anchored in two foundational narratives: Ethereum scaling and privacy-preserving computation. ZK acceleration networks and ZK mining are key strategic focuses due to their stable game-theoretic structures.

● Institutions view new public blockchains primarily as strategic allocations rather than high-conviction, immediate opportunities. They are closely tracking two innovations from recent chains: the Move programming language and parallelized execution technology—both seen as potentially more valuable than any single chain.

● Middleware ranks third in institutional interest, behind ZK and new public blockchains. Key subcategories include decentralized identity (DID), data protocols, and wallets.

● Institutions continue to monitor DeFi but remain broadly cautious. For existing protocols, only those generating stable cash flows without relying on subsidies are considered candidates for renewed growth. For new DeFi protocols, institutions favor those operating in mature traditional finance niches with few on-chain competitors, most of which fall under derivatives.

● The debate around social projects stems from a shared belief that social interaction is a fundamental user need with massive potential, yet many institutions see current SocialFi projects as early-stage, with unclear business models and no proven sustainable paradigms. Relying solely on tokenomics or superficial Web2 rebranding is unlikely to draw users away from established tech giants.

● The gaming debate centers on two opposing views: many acknowledge gaming's unmatched ability to attract new users, while others argue that current blockchain gaming models are fundamentally unsustainable.

We believe infrastructure—including ZK, new public blockchains, and middleware—holds the most promise. Application-layer sectors face greater uncertainty: DeFi has a relatively higher probability of success, especially in derivatives. Social remains premature, needing more foundational development before reaching its potential. Gaming offers growth opportunities, but projects with superior economic models have the greatest upside.

1. Current State of Investment Activity

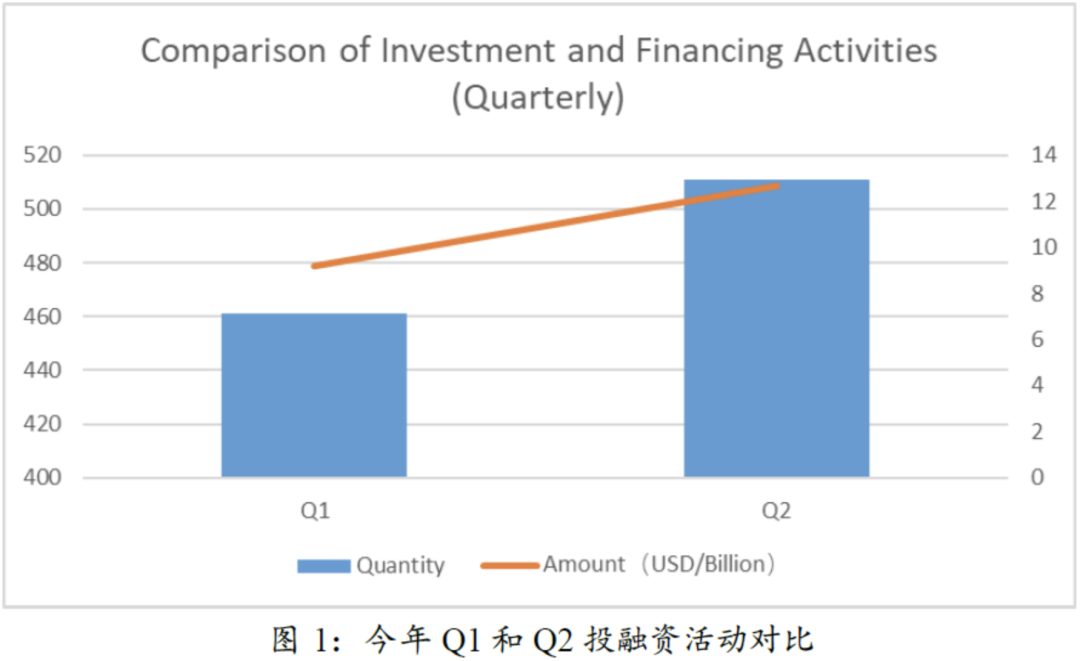

First, let's examine the current state of global crypto investment. According to publicly reported data from Odaily and PANews, the global crypto market recorded 511 funding events (excluding fund-raising rounds and M&A) in Q2 2022, with total disclosed funding of $12.71 billion. Among these, 28 deals exceeded $100 million each.

Compared to Q1 2022: the global crypto market saw 461 funding events with $9.2 billion in disclosed funding. Despite worsening secondary-market conditions in Q2, investment activity showed signs of recovery: deal count rose 11% quarter-on-quarter, and total funding increased 38%.

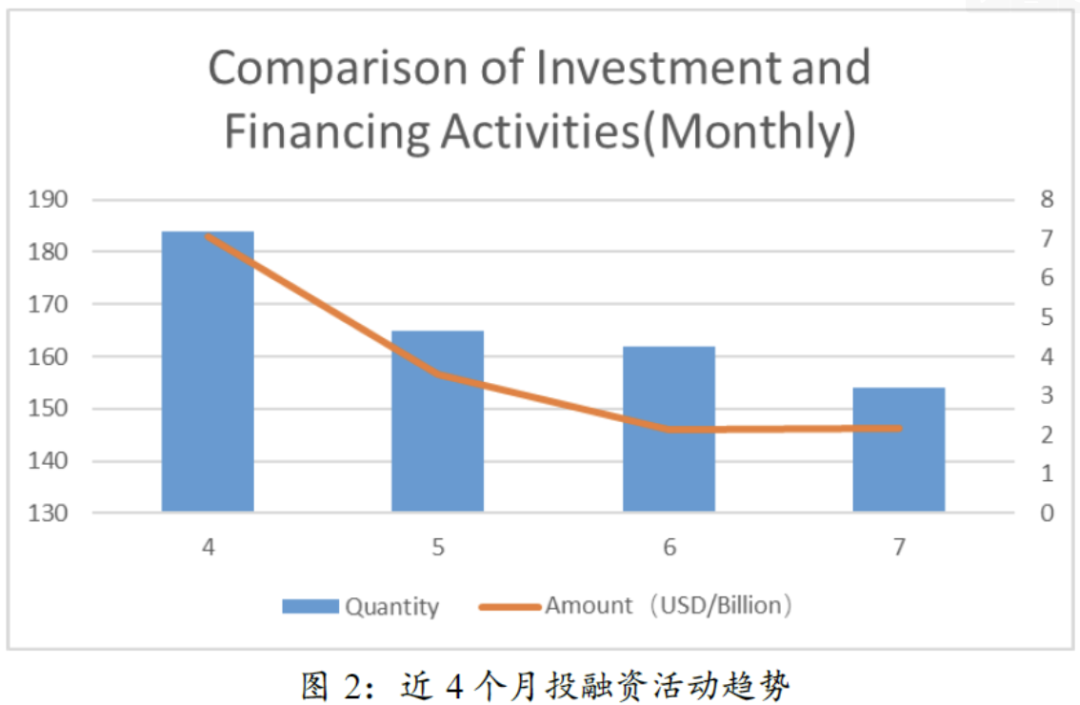

However, monthly trends reveal a cooling pattern. From April to July, both the number and total value of funding events declined steadily. Over these four months, total disclosed funding dropped nearly 70%, while deal count fell 16%. This subdued climate aligns with the cautious sentiment expressed by interviewees.

The divergence between quarterly and monthly trends may stem from a secondary market rebound from January to March, which boosted investor confidence and led to a wave of funding announcements in April. Conversely, the collapses of Terra and Three Arrows Capital (3AC) severely damaged market confidence, prompting heightened caution and declining deal volume and value from May through July.

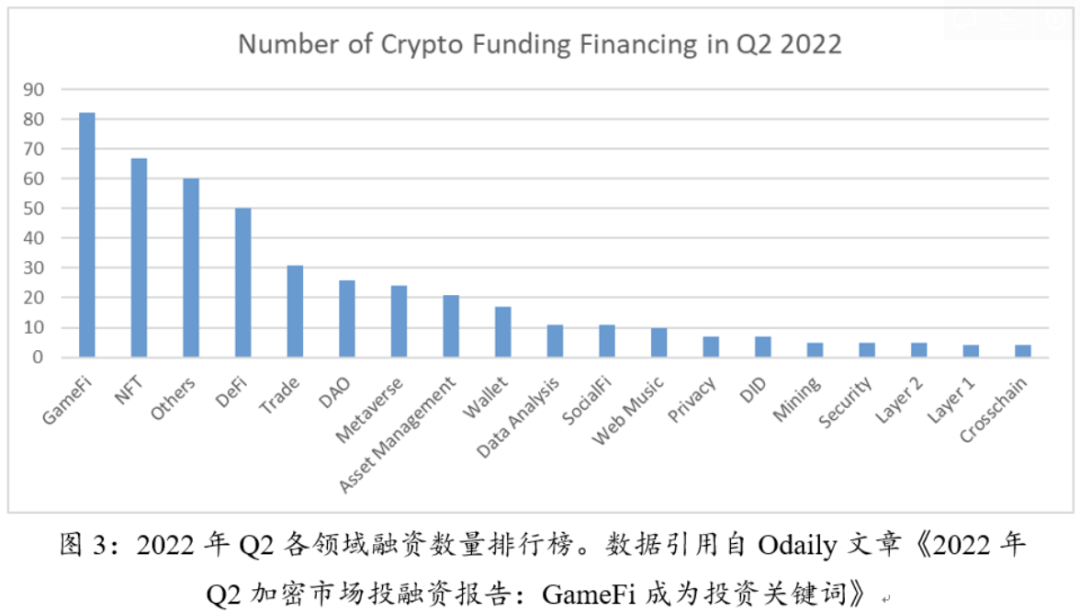

Next, let's review which sectors investment institutions prioritized previously. As shown below, GameFi and NFT were the top two focus areas for global crypto investment institutions in Q2. Gaming, gaming-related infrastructure, and technical solutions collectively secured 82 funding rounds—the highest count, representing 16% of all deals. GameFi also led in funding value, raising $2.996 billion, or 23.5% of the total. NFT projects ranked second with 67 deals. DeFi ranked fourth with 50 deals. Infrastructure categories—including L1/L2, mining, privacy, and identity—formed a "long-tail" segment, each attracting roughly 10 funding rounds.

As the crypto industry evolves, investment priorities have shifted markedly in just two months. Let's hear directly from the institutions we interviewed.

Huobi Research's survey included over 20 investment firms—spanning crypto-native top-tier funds, crypto divisions of traditional investment firms, investment arms of crypto conglomerates (e.g., exchanges, wallets, asset managers), incubation-focused firms, and sector-specialized investors. By diversifying our interviewee pool, we aimed to obtain a more comprehensive and realistic understanding. In these interviews, we discussed participants' analyses of current conditions and future outlooks across various sectors, along with their investment logic and strategies—hoping to offer readers deeper insight into the cryptocurrency industry.

2. Sector Potential Rankings and Investment Rationale

We aggregated the sectors highlighted by participating institutions and ranked them by frequency of mention, as shown below. Some categories overlap conceptually; detailed analysis per domain follows later—this chart provides an initial visual overview.

Institutions' top focus areas fall into two broad categories: infrastructure and applications. Overall, infrastructure receives stronger attention. "Infra" ranks highest in mention frequency—with ZK and new public blockchains forming two primary themes. Categories like middleware, data, oracles, and DID also carry clear infrastructural characteristics. Among application-layer projects, DeFi, GameFi, and social rank top three. Although DeFi has been relatively quiet recently, it remains the most favored direction among institutions. In contrast, gaming and social draw sharply divided opinions—some institutions strongly endorse them, while others express clear skepticism. Below, we analyze each area to understand why institutions prioritize them.

2.1 Infrastructure

Survey results show institutions consistently prioritize infrastructure over applications. While some did not explicitly use the term "Infra," their focus centered on areas like ZK and new public blockchains. For analytical clarity, this report groups zero-knowledge proofs, new public blockchains, middleware, DID, data, modular architectures, and related fields under the umbrella of infrastructure.

Why Infrastructure Matters

Two main reasons drive this emphasis on infrastructure: first, aligning with the industry's natural development cycle; second, preparing for Web3's next narrative wave.

First, aligning with the industry's development cycle—not the typical bull/bear cycle, but rather the cyclical rotation between infrastructure and application layers.

IOSG Ventures uses the "Newton's cradle" principle to describe this dynamic. They argue that for any emerging tech sector to achieve widespread adoption, it first needs robust underlying infrastructure. Only when the infrastructure matures can it support the first wave of applications (for instance, the earliest DeFi apps wouldn't exist without Ethereum's smart contracts). In turn, as these applications grow and evolve, they demand even higher-performance infrastructure and more sophisticated middleware or specialized app chains—creating a feedback loop that drives further infrastructure development (e.g., increasingly complex DeFi protocols on Layer 2 require stronger base-layer performance, pushing Rollup tech forward; today's crypto GameFi and SocialFi ecosystems are still nascent, each needing its own dedicated infrastructure). This cyclical, perfectly elastic interaction mirrors a Newton's cradle.

Following this logic, an initial phase of "fat protocol, thin application" emerges, where protocols capture significant token value before applications do. In practice, IOSG spent five years building its portfolio in the protocol and infrastructure (Infra) layer. At Layer 1, they invested in projects like Cosmos, Polkadot (DOT), Near, and Ava Labs; at Layer 2, they backed Starkware and Arbitrum; and in middleware, they made substantial bets on native developer protocols. As infrastructure matures and stabilizes, IOSG has pivoted toward a "fat application" strategy—targeting potential unicorns in DeFi and gaming/social sectors, including MetaMask, 1inch, Project Galaxy, CyberConnect, Bigtime Studio, and Illuvium.

Bixin Ventures believes that few application-layer products today show strong innovation, with many hyped concepts still unproven—making it too early to focus investment there. Instead, they see the current moment as ideal for investing in infrastructure, anticipating that these foundational projects will lead the next bull market. Compared to betting on application projects, infrastructure investments offer a higher probability of success[1]. They also provide significant upside potential and can absorb much larger amounts of capital. Matrix Partners proposes a practical "80/20 Rule" as a guideline: during bear markets, allocate 80% of research effort to infrastructure and 20% to applications; during bull markets, reverse the ratio.

The second reason is to prepare for Web3's new narratives. The most ambitious vision in today's internet landscape is Web3, with major traditional giants—including Amazon, Google, Meta, ByteDance, and Baidu—actively exploring and deploying in this space. A common view defines Web3 as a next-generation internet ecosystem built on blockchain technology. Crucially, this system must serve not millions, but billions of users. Current blockchain infrastructure is far from ready to support adoption at that scale, necessitating continuous upgrades and overhauls.

On assessing infrastructure value, Cobo Ventures and Foresight Ventures emphasize its technology-driven nature. Investors should prioritize technological advancement and maturity, seeking solutions that are low-cost, efficient, and secure. Equally important is evaluating the vitality of the developer ecosystem and the level of user adoption—only then can real-world value be created.

Below, we examine each firm's perspectives and analytical frameworks for several key infrastructure domains.

2.1.1 Zero-Knowledge Proofs

Zero-knowledge proofs (ZK) are the most closely watched infrastructure domain across all firms surveyed, primarily encompassing ZK Rollups and their acceleration networks.

The Status of ZK

Two comparisons help illustrate ZK's standing among institutional investors.

First, within the Layer-2 domain, ZK has effectively become synonymous with Layer 2 and is clearly favored over Optimistic (OP) Rollups. Currently, Rollup is the dominant Layer-2 technology, with two main paths: Optimistic Rollup and ZK Rollup. In interviews, nearly every firm discussing Layer 2 expressed exclusive confidence in the ZK Rollup path, expressing skepticism—or outright dismissal—of OP Rollup, despite OP's stronger metrics in several areas. Multiple firms characterized OP as viable only for the short-to-medium term, lacking strong long-term value. In contrast, they see ZK's role in cryptography and blockchain as analogous to machine learning in AI: a central, foundational technology and one of the industry's top narratives.

Second, in the public-chain competitive landscape, institutional enthusiasm for ZK slightly exceeds that for new Layer 1s. This is because ZK—or the Layer-2 paradigm it represents—embodies Ethereum's scaling roadmap, and institutions currently show a stronger preference for Ethereum. JDAC Capital posits that Ethereum will evolve into a settlement layer whose user base could expand beyond crypto-natives—even traditional internet services might leverage it for settlement. Given Ethereum's high asset quality and strong network consensus, settlements conducted on it enjoy greater trust and broader recognition of asset value.

Rationale for Investing in ZK

Beyond comparative advantages, ZK's intrinsic value is compelling. Zonff Partners explicitly states that ZK is one of four potential core drivers for the next cycle, possessing long-term value. It anchors two top-tier narratives: Ethereum scaling and privacy-preserving computation. Much like machine learning's role in AI, ZK Proofs may hold a similarly pivotal position in cryptography and blockchain—especially in Ethereum scaling, where the value chain already shows structural completeness, including developers, compute hardware providers, node services, application demand, and end-users. A structurally stable sector is well-suited for institutional capital, offering predictable, steady growth less dependent on macro conditions or fleeting hype. This allows entrepreneurs and projects to generate positive feedback more readily during execution.

First, ZK Rollups will play an increasingly critical role in Ethereum scaling—their full potential remains untapped. The performance benefits are clear, but ZK also addresses blockchain "lightweighting." Full nodes must store large amounts of data, burdening typical node operators and exacerbating centralization. ZK Rollups drastically reduce on-chain data uploads, easing node storage pressure. As on-chain ecosystems grow richer and more active, demand for lightweight solutions intensifies—expanding ZK Rollup's addressable market. (Of course, raw transaction data still needs storage—this is where modular blockchains' data availability layers come in.)

Second, ZK holds promise for solving broader privacy challenges. Before DeFi and NFTs, on-chain data volume was limited, making privacy less urgent. With little to protect and no clear mechanisms, privacy discussions remained theoretical. But DeFi's rise made privacy a critical priority. There's no justification for mandating universal on-chain transparency—especially for whales and institutions whose activity reflects substantial economic interests. Today's analytics tools amplify blockchain's inherent transparency, creating real friction for these actors. Thus, privacy demand is both genuine and growing deterministically. As on-chain data volume grows exponentially, this demand will only intensify. Yet no superior privacy solution exists today. Beyond ZK, homomorphic encryption and MPC also present opportunities.

Based on this logic, multiple firms consider ZK Rollup the optimal Layer-2 solution. Furthermore, given the Ethereum Foundation's explicit endorsement of ZK technology and the lack of comparably advanced alternatives, investing in its foundational layers is seen as essential.

Key Investment Focus Areas for ZK

Zonff Partners, JDAC Capital, and Hashkey Capital all explicitly express active interest in ZK acceleration networks and ZK mining. Generating ZK proofs demands significant computational resources, creating genuine hardware-acceleration demand. Coupled with ZK's overarching strategic importance, ZK mining represents a long-term, structural need.

What institutions value most is ZK mining's structural positioning within the broader industrial chain.

The ZK value chain resembles Bitcoin mining: upstream includes chip manufacturers, hardware vendors, node operators, and mining pools; downstream comprises developers and diverse applications—forming a stable, balanced structure. Currently, upstream ZK projects—including Scroll, zkSync, Starknet, Aztec, and Polygon—use fragmented technical approaches, making large-scale institutional allocation challenging due to the difficulty of identifying high-value, cost-effective targets. Investing in these infrastructure components carries inherent risk—even an element of speculation. Meanwhile, downstream applications—following the DeFi Summer and gaming boom—currently lack obvious breakout directions, and competition within verticals remains fierce. Institutions face a similar selection dilemma: first picking the right sector, then the winning project—a statistically improbable feat. ZK mining sits between these extremes, offering structural arbitrage. When both upstream (technical approaches) and downstream (applications) are highly fragmented, the middle layer provides stable-return opportunities—akin to selling bottled water and jeans to gold prospectors.

However, the ZK hardware industry is unlikely to reach Bitcoin mining's market scale. First, it depends on whether ZK base-layer protocols adopt open, decentralized proof generation (i.e., mining)—centralized alternatives remain viable. Second, and more critically, ZK mining's scale is constrained by the overall size of ZK-based projects—how much capital the ZK ecosystem can ultimately absorb. Should this constraint see major breakthroughs, ZK mining's ceiling could rise substantially.

Impact of ZK’s Rise on Other Sectors

Finally, let's examine how ZK's rise interacts with other sectors.

First, ZK will strengthen Ethereum's competitiveness. JDAC asserts that Ethereum's technical architecture and community-building capabilities are unmatched by other L1s—even EVM-compatible chains struggle to challenge its dominance.

As ZK technology matures, it will further cement Ethereum's dominance. While it's too early for definitive conclusions, we can reasonably expect ZK to significantly boost Ethereum's competitive edge. The "Iron Throne" of public blockchains isn't easily challenged. Even during last year's bull market—when Ethereum's Layer 2 solutions were still nascent and rival L1s offered negligible fees—Ethereum still held over 60% of the total value locked (TVL). If Ethereum can close the performance gap with other L1s while preserving its high degree of decentralization, its lead is likely to grow even stronger.

Second, ZK will fuel demand for the Data Availability (DA) layer. As mentioned earlier, while ZK Rollups post minimal data on-chain, they still need to publish raw transaction data. The DA layer stores this data and ensures its availability. In this sense, the DA layer acts as an upstream industry for ZK—ZK's growth will directly drive the DA layer's expansion.

In a previous article titled "How the Data Availability Layer Can Shape the Future of Blockchain," the author estimated that if Rollups achieve mass adoption—creating a "Rollup-centric" ecosystem—and ETH's price rebounds strongly, the DA layer could generate up to $2 billion in annual revenue.

Third, ZK's rise is unlikely to disrupt analytics tools significantly. Currently, ZK Rollups are primarily focused on scalability; privacy-oriented projects exist but aren't mainstream. Privacy remains a longstanding yet under-prioritized field, even in traditional internet ecosystems. Privacy protection comes at a cost, and if that cost stays too high, it could deter smaller users and reduce network utility. Most users still prioritize convenience and low fees above all. Therefore, the author believes ZK's development, at least in the near term, won't undermine the core viability of analytics tools—both sectors can evolve in parallel.

Fourth, ZK's advancement could catalyze new application-layer projects. Because ZK Rollups require uploading only tiny amounts of data, applications can implement far more complex business logic. This could give rise to novel applications—such as DeFi protocols with significantly more intricate rules—or even the next "killer app" on Layer 2, likely emerging first on ZK Rollups. However, this depends on one key prerequisite: the maturity of general-purpose ZK-EVMs.

2.1.2 New L1 Blockchains

New L1 blockchains also attract considerable attention, though institutional investors discuss them far less than zero-knowledge proofs. Much of this interest is strategic and portfolio-driven, rather than based on clear, high-conviction opportunities.

Rationale for Investing in New L1s

Public blockchains remain a perennially dominant sector in crypto investing, with an exceptionally high ceiling. Each wave of new L1s brings a partial paradigm shift—for example, the transition from PoW to PoS consensus has driven long-term industry evolution. Such shifts present massive opportunities: solving the "blockchain trilemma" could even overturn current logic and challenge Ethereum's throne. Yet truly disruptive opportunities are rare. Major paradigm shifts are exceedingly difficult to achieve—they demand extraordinary innovation, requiring solutions at least 10x better than existing ones. Multiple institutions note that no current project meets this bar. Still, the future blockchain landscape will likely remain multi-chain. A new L1 doesn't need to capture massive market share to succeed—it merely needs a viable user base and capital inflows, enabling meaningful market-cap growth during bull markets and making it an attractive investment.

When evaluating projects, several venture capital firms emphasize the importance of assessing performance correctly. First, *comparative* performance matters more than raw metrics. Every new generation of L1s touts improved performance—almost exclusively measured against Ethereum. Yet Ethereum itself keeps improving, and once Layer 2 gains wider adoption, end-users may barely notice performance differences between L1s, or find them insufficiently compelling. Second, real-world performance outweighs lab benchmarks. Aptos' claimed 160,000 TPS is a lab figure—and requires careful analysis of transaction dependencies to fully leverage concurrency. Its actual throughput remains unproven. Solana claims 65,000 TPS but has suffered multiple major outages, revealing inconsistent stability.

Highlights of New L1s

Although no single project stands out as overwhelmingly compelling, HashKey and NGC Ventures highlight two key innovations among recent new L1s. The first is the Move programming language, adopted by leading L1s Aptos and Sui. The second is parallelized transaction processing. Their significance may extend far beyond any individual chain—potentially reshaping the entire industry.

The Move language is a standout innovation—its value may surpass that of the headline-grabbing L1s themselves. Move introduces "resource-oriented programming," abstracting a new primitive called a "resource." Developers can easily define any resource type (e.g., common crypto assets are resources that cannot be duplicated or destroyed) and precisely specify how each resource can be manipulated. This offers several key advantages:

First, Move provides higher smart contract security. By decoupling resource definitions from access control, and incorporating static typing, generics, modular architecture, and formal verification, Move makes smart contracts inherently safer for asset-centric use cases—securing digital assets at the contract level.

Second, Move allows developers to focus on higher-value concerns—like implementing correct business logic and robust access-control policies.

Third, Move-based smart contracts offer stronger composability—reducing on-chain storage needs and simplifying optimization and upgrades.

Fourth, Move has a gentler learning curve than Solidity—and its underlying compiler tooling further lowers the barrier to entry. Even if Move-based L1s underperform, they'll serve as valuable educational tools for future developers. If successful, Move could usher in an entirely new programming paradigm. Viewed this way, Move's intrinsic value exceeds that of any specific L1 built on it.

Parallelized processing is another major highlight—and may signal a foundational architectural shift. Today, Ethereum processes transactions sequentially, relying on a single-core EVM. Parallelized transaction processing abandons linear execution for concurrency—for instance, Aptos uses a 16-core CPU to run multiple threads handling unrelated transactions simultaneously, boosting TPS. Sharding is a classic form of parallelism but operates at the system architecture level. Here, "parallelization" refers specifically to process- or thread-level concurrency in software execution—closer to the system's core. In the future, parallelization may become standard across all L1s, with varying degrees of implementation—similar to how PoS consensus became ubiquitous across new L1s after 2018–2019, largely replacing PoW.

2.1.3 Middleware

Middleware ranks third in investor attention, behind ZK and new L1s. Middleware generally refers to software that provides universal services and functionality to applications; typical responsibilities include data management, application services, messaging, authentication, and API management. It bridges infrastructure and applications. For analytical clarity, this article classifies middleware under the infrastructure category.

Given middleware's infrastructural role, widespread adoption by applications creates powerful network effects—early adopters attract others, eventually establishing de facto standards. Consequently, these sectors naturally draw intense investor interest. Key focus areas include decentralized identity (DID), data protocols, and wallets.

Decentralized Identity (DID) serves as a user-owned and controlled internet address—essential infrastructure for many Web3 applications. While users already own their on-chain assets, their digital identities remain underdeveloped. Just as decentralized assets can move freely between applications, users should have portable, self-sovereign identities. Such identities would enable social applications, non-financial Web3 apps, and novel DeFi use cases. For example, in a social app, users could prove credentials—like having used a specific DeFi protocol, participated in DAO governance, or played a certain game—to find like-minded peers. Yet investors also scrutinize whether DID protocols can generate sustainable revenue. So far, few have demonstrated viable models—most rely on staking rewards or liquidity mining, which are unsustainable. Long-term, monetization via service fees becomes feasible once a critical user base is established—but building that base demands patience and long-term commitment from founding teams.

Regarding data protocols, investors prioritize two traits above all: precise privacy delineation and rapid responsiveness. EVG notes that virtually no existing protocol clearly defines which data types should remain private versus publicly accessible. For instance, identity information is typically confidential—but what about specific datasets? Should the protocol own them, allowing open retrieval and audit? Striking this balance is critical—and protocols that solve it decisively may emerge as winners. Another priority is speed and high-frequency response, especially given hedge funds' need for real-time data to inform trading decisions. Protocols like Dune and The Graph are already highly capable—but demand even greater timeliness.

For wallet middleware, expanding user reach is paramount. Most non-crypto-native users have never used a crypto wallet—and wallets often represent their first barrier to entering the ecosystem. StepN set a strong precedent by embedding a Web3 wallet directly into its product: guiding newcomers to create wallets seamlessly during account registration, delivering a frictionless first-wallet experience. This approach offers wallets a fresh strategic path—achieving organic, invisible user acquisition through deep integration with consumer-facing dApps.

2.2 DeFi

As the pioneering application-layer sector, DeFi naturally sparks extensive discussion. Yet beyond incremental AMM algorithm refinements, DeFi has seen little fundamental innovation—"nested" improvements rarely generate significant market resonance. Like public blockchains, institutions tend to monitor DeFi continuously but overall remain in a wait-and-see stance.

Rationale for Investing in DeFi

Blockchain technology has been intertwined with finance from the very beginning. The advent of smart contracts unlocked DeFi, which has since demonstrated remarkable financial innovation and attracted significant capital. DeFi's composability and permissionless nature directly tackle core issues in traditional finance, such as high barriers to entry, centralized control, and large capital requirements. Transactions on-chain are transparent and public, preventing unauthorized asset seizure. Anyone can interact with on-chain liquidity and positions. Smart contracts encode the rules for financial instruments and protocols, enforced automatically and impartially by code. Following the repeated failures of centralized finance (CeFi) institutions, the advantages of DeFi have become even more apparent.

Development Trajectory

Since the rise of Automated Market Makers (AMMs), the DeFi market has matured considerably. It now features diverse verticals and relatively robust ecosystems. Major infrastructure projects—including DEXs and lending protocols—have established clear network effects. Institutions like Nothing Research and Matrix hold the following core views on DeFi's trajectory:

For established DeFi protocols, the immediate priority is surviving the bear market. The initial growth of DeFi was heavily fueled by subsidies and compelling narratives to capture market share. However, this model isn't sustainable. In a downturn, only protocols that generate stable cash flows and can reduce reliance on subsidies are positioned for a future comeback. Furthermore, many functionally sound protocols have tokens that fail to capture ecosystem value, leading to weak token prices that hinder further development. Protocols that successfully optimize their tokenomics may experience a second wave of growth.

For new DeFi protocols, most verticals are already crowded. Without a paradigm shift in the broader macro environment, finding untapped "blue oceans" is extremely difficult. Consequently, institutional focus has shifted to DeFi protocols operating in traditionally mature sectors with few on-chain competitors, particularly derivatives. While some derivative protocols have promising models, market education remains a hurdle. Beyond organic user adoption during bull markets, these protocols need strong operational execution to attract incremental users.

2.3 Social

The social sector remains a hot topic, though institutional perspectives on its near-term potential vary widely.

Rationale for Building Social Infrastructure

On one hand, there is broad consensus on the foundational importance of social interaction—a core human need that enables connection, value exchange, and collaboration. Web3 social is seen as an inevitable trend with a high ceiling. Cobo Ventures believes that in the Web3 era, users will gain absolute control over their social data. SocialFi products, built on Web3 infrastructure, merge the demand for decentralized social experiences with decentralized finance. This breaks platform monopolies, eliminates single points of failure, and creates novel business models within the global digital economy.

On the other hand, institutions diverge on near-to-mid-term execution. Huobi Incubator argues that current SocialFi projects are still nascent, lacking sustainable models and clear roadmaps. Crucially, simply adding tokenomics or repackaging Web2 social features won't meaningfully compete with established giants. A deeper exploration of Web3-native user traits and needs is essential. From this view, SocialFi currently lacks the conditions to be the primary catalyst for the next bull market.

Development Trajectory

Based on multiple interviews, we can categorize projects leveraging blockchain and tokenomics for social interaction as follows:

First, Blockchain + Social: Addressing Web2 Shortcomings

The core aim of some projects is to challenge traditional social media giants by leveraging blockchain's unique properties:

Data sovereignty: On traditional platforms, users are merely data consumers. Blockchain enables on-chain data storage, giving users full control.

Data interoperability: Web2 suffers from walled gardens where data is siloed and non-portable.

Data privacy: Unlike Web2's passive privacy risks, blockchain data is public but can be selectively encrypted (e.g., via wallet addresses), allowing users to control what they share.

Economically, issuing platform tokens to reward users is a natural step. Tokenomics can reshape the user-platform relationship: the more users contribute, the greater their rewards, potentially increasing the token's value. Models like "X2Earn" and content mining introduced new incentives, briefly fueling a SocialFi boom.

While tokenomics can bootstrap a project, fostering genuine social interaction and creativity cannot rely on financial incentives alone.

SocialFi faces significant challenges:

Small user base: The native Web3 social user pool is limited, and token incentives are inefficient at converting Web2 users.

Tokenomic backlash: Token-based rewards are time-sensitive. Cash provides immediate value, while token values fluctuate. When prices fall, user incentives erode, creating a negative feedback loop.

Fuzzy user profiling: Over-emphasizing the "Fi" in SocialFi attracts speculators who leave when profits dry up, making it hard to identify and serve genuine social users.

Inadequate infrastructure: Current infrastructure struggles to support the data-intensive needs of complex social applications.

Second, Exploring Web3-Native Social

The focus is shifting towards serving Web3-native users and building foundational layers for identity-based communication and relationship-building.

· Web3 Identity

Sustainable progress requires stable infrastructure. More projects are building Web3 identity systems to map real social cohorts. Identity graph construction involves two steps:

Data parsing: Unlike Web2 apps that must build user habits from zero, Web3 on-chain data is public and reusable. Projects can leverage existing data—like transaction history or NFT holdings—to construct identifiable user profiles.

Identity aggregation: While data parsing is open, empowering users to actively aggregate their multi-chain, multi-address, and even off-chain data enables richer, more precise identity modeling, which is key for long-term project viability.

· Information Dissemination

This can be categorized into two types:

Non-targeted dissemination: Primarily uses social media formats—publishing content (text, images, video) to attract a broad audience.

Targeted dissemination: Sending messages to specific addresses or groups, useful for NFT OTC trades, hacker negotiations, or project airdrops.

· Relationship Formation

Once connections are made, forming social relationships—strong ties, weak ties, temporary links—follows. Web2 apps connect users via centralized platforms, making it hard to monetize weak ties. Web3 introduces tokens, adding an economic layer to social behavior and allowing weak ties to solidify through transactions.

Overall, after early experimentation and the SocialFi hype cycle, the sector is gradually finding sustainable paths. As social data, network graphs, and other foundational infrastructure mature, genuine social needs will be better served, bringing Web3 social closer to reality.

2.4 Gaming

In terms of user demand, gaming is similar to social apps—it's a common, everyday application. The key distinction is that the 2021 gaming wave, led by Axie Infinity, showed that blockchain games can create their own momentum while also achieving significant premiums on secondary markets through token-based "play-to-earn" (P2E) mechanics and profit incentives. However, this boom was short-lived. As leading projects cooled, bearish narratives around GameFi became widespread, keeping it at the center of controversy. Our research confirms that GameFi remains a highly debated topic.

The Case for On-Chain Gaming

There's broad consensus among institutional players on why games should be built on-chain. Animoca Brands and Huobi Ventures have provided detailed analyses, which we summarize here:

Blockchain gaming enables true digital ownership for players, facilitates decentralized trust, and allows asset portability—making games more sustainable.

Gaming naturally creates diverse trading scenarios. Gold farming and open markets already exist in traditional MMORPGs and PC games, with established regulatory mechanisms and design logic both on and off-chain. The circulation of in-game items and currency is a well-defined need. Secondary markets in traditional games are often stifled by corporate restrictions, leading to a poor user experience. Blockchain technology changes this, benefiting both studios and players. Currently, studios mainly earn from cosmetic sales, leaving the massive potential of secondary markets untapped. Studios can generate recurring revenue through transaction fees, while players gain more freedom to create, explore new gameplay, and increase engagement—ultimately enhancing the game's value and their willingness to spend.

The multifaceted utility of unique in-game assets—for trading, speculation, and collecting—aligns perfectly with NFTs. Many items are one-of-a-kind, varying in rarity and function, making their tokenization as NFTs a natural fit.

Gaming acts as both a traffic gateway for L1 blockchains and an experimental sandbox for L2 solutions. GameFi is currently the most active and practical trading sector in crypto. In 2021, its role in driving public chain adoption gained attention. However, Ethereum's TPS limitations can't meet gaming's real-time demands, pushing high-performance L1 chains to seek new opportunities. Meanwhile, L2s lack high-activity, rapid-settlement applications—exactly where gaming fits. Their future evolution could be symbiotic.

From these perspectives, gaming holds exceptional long-term investment value. Yet current GameFi development models face criticism, especially around sustainability. Most follow a "flash-in-the-pan" pattern: short-term, fast-paced P2E mechanics attract quick capital, amplified by FOMO-driven growth. In the long run, many GameFi economic models are fundamentally unhealthy, even Ponzi-like. As novelty fades, momentum drops, making it hard to attract new users. Imbalanced economics encourage early beneficiaries to cash out, depreciating in-game assets and accelerating the project's decline. When the game dies, its assets die with it—whether stored on-chain or on centralized servers.

Two approaches could solve this. First, make games genuinely fun—and keep them that way. Second, build healthier economies: establish stable, game-driven strategic interactions among players based on win/loss outcomes or functional roles—not on perpetual growth that forces new entrants to absorb prior losses. At least one method must succeed for game-based assets to gain lasting value, fostering durable consensus and viable trading logic.

The GameFi Development Path

Using Maslow's hierarchy of needs, humans satisfy basic physiological and safety needs before pursuing higher-order ones like social belonging, esteem, and self-actualization. Gaming fits into higher-order needs and remains an early-stage sector in blockchain. Ethereum is only about a decade old; application growth started with DeFi Summer in 2020, followed by GameFi's breakout led by Axie Infinity a year later. Bull market exuberance accelerated GameFi's premature rise: primary markets wanted fresh narratives, secondary markets craved new mechanics, and conditions forced rapid adoption. As enthusiasm cools, we can now reassess the sector—acknowledging its flaws while affirming its long-term potential as a killer app built on infrastructure, full of latent opportunities.

1. Opportunities from Game Teams

First, traditional Web2 gaming giants. News of established studios embracing Web3 is increasingly common. These veterans bring deep expertise and abundant resources in publishing, live ops, monetization, and advertising—often capable of developing and operating multiple titles simultaneously. Their entry into GameFi could yield not just single games but entire portfolios, leveraging existing user bases for gradual conversion and injecting meaningful new users into the ecosystem. While this approach drives effective user growth, it involves slower development and operational timelines, requiring sustained, long-term commitment.

Second, crypto-native game studios. Some teams within the crypto industry are building blockchain games, but game development has high barriers. Even if they recruit talent from top Web2 studios, they lack access to those studios' operational infrastructure and distribution channels, making it hard to replicate past success. Consequently, some teams focus on innovating tokenomics instead. A robust economic model should foster rich strategic interplay—where players earn rewards from others' participation, not just extract value from the protocol. As Foresight Ventures argues, for GameFi, economics is the "1", while gameplay is the "0". Native teams can't outcompete traditional studios on pure gameplay quality, so superior tokenomics must come first.

2. Opportunities from Game Models

Whether Axie Infinity's P2E model or StepN's broader X2E (e.g., "move-to-earn") paradigm, these GameFi variants are essentially generalized DeFi products—their core innovation lies in tokenomics, not gameplay. Fundamentally, P2E and X2E are liquidity mining schemes with extra steps: novel token distribution mechanisms without intrinsic competitive advantage. Moreover, as noted, current tokenomic models remain structurally unsound. Looking ahead, GameFi's true value will stem from gameplay depth and innovative crypto-native design. SevenX identifies three game types most likely to break through first: (1) simple games that lower entry barriers to expand player bases; (2) highly competitive games that foster long-term retention through "the joy of striving against others"; and (3) games with optimized economic models that allow a subset of players to earn sustainably, achieving endogenous ecosystem circulation.

Overall, from an investment standpoint, GameFi's primary market carries elevated risk. In traditional Web2 gaming, studios conduct extensive market research and testing before launch—costs in manpower, resources, and capital that crypto-native teams can't bear, especially given time constraints. Crypto's extreme cyclicity ties profitability tightly to macro market conditions. Prioritizing genuine gameplay quality demands elite, specialized teams and inevitably lengthens development cycles. This tension amplifies both investment risk and opportunity cost.

Conversely, crypto-native investment firms often prioritize rapid monetization—a dynamic that pressures GameFi teams to focus on short-term value extraction. Hence, many GameFi projects claiming 1–2 year development timelines face industry skepticism.

Additionally, by nature, all games have finite lifespans. A game's core genre is fixed at inception, making iterative updates difficult. Investing in GameFi thus resembles a "one-shot deal." Until these structural challenges are resolved, institutions remain cautious—preferring to watch rather than act.

3. Where Do Future Opportunities Lie?

Having analyzed these domains, we naturally ask: Which projects will explode in the next bull cycle? In which sectors will they emerge? And what strategies will best capture these opportunities? Below are our forward-looking views—not investment advice.

Infrastructure Outlook and Strategy

Based on sector rotation cycles, infrastructure is poised to become (and arguably already is) crypto's next major protagonist.

ZK mining represents a high-probability, high-upside opportunity. Like Bitcoin mining, it's unlikely to centralize significantly, offering relatively stable returns. Its market potential is vast: though optimal hardware paths (GPU/FPGA/ASIC) remain uncertain, GPUs and FPGAs retain strong residual value and high fault tolerance. Two leading ZK Rollup platforms—StarkNet and zkSync—dominate today, yet industry competition is unresolved. This ambiguity creates immense opportunity. Based on technical strength and funding traction, we remain most bullish on these two leaders—though StarkWare's current valuation appears stretched, presenting potential risk.

New L1 blockchains are experiencing a "golden age of fragmentation"—a low-probability, ultra-high-upside sector. Still in early stages and compounded by overall market lethargy, they haven't yet reached breakout timing. Investors have ample runway to study their innovations and engage directly with communities, witnessing ecosystem growth firsthand. Since half a public chain's value comes from its ecosystem, spotting several high-quality or uniquely differentiated projects on a chain meaningfully increases conviction in its long-term success.

Middleware mirrors new L1s: similarly low-probability, high-upside. Here, upstream/downstream partnerships matter most. For middleware, market leaders enjoy stronger durability—warranting close monitoring. Before industry consolidation clarifies, index-style allocation is advisable over betting on any single project.

Application Outlook and Strategy

DeFi still holds enormous potential for the next bull market. It remains a high-risk, high-reward sector with a low success rate. In the current bear market, DeFi activity has slowed, entering a dormant phase. While some blue-chip projects may endure across cycles, their next growth spurt will likely depend on improved blockchain performance, coupled with innovative mechanisms or expanded use cases. Future DeFi innovation is expected to focus on derivatives built on Layer 2 or emerging blockchains. Within derivatives, perpetual contract volumes still lag far behind centralized exchanges, indicating significant room for growth. As the market recovers, long-term demand and narrative around undercollateralized lending and algorithmic stablecoins persist, offering potential opportunities. However, following the collapses of UST and 3AC, these areas need to evolve. Given DeFi's high growth potential and concentrated nature, investors should primarily focus on leading projects.

Social applications are another high-risk, low-probability sector. Their development hinges on foundational infrastructure like on-chain identity solutions, better blockchain performance, and broader real-world utility. As a result, social may be one of the later narratives to gain traction. Simply replicating existing Web2 models is unlikely to create a breakthrough or compete with traditional social giants. However, blockchain-based social apps aren't without merit. They could find their niche in areas like fulfilling native on-chain needs—such as targeted information dissemination and community building—or by using tokenomics to address real social pain points, like trust within interactions.

Gaming carries high odds and a better chance of success than social, with room for numerous small to mid-sized projects. As more major studios enter the space, they will bring incremental users, fueling overall sector growth. This makes gaming a strong candidate to explode in the next bull market. "Fun" may not be the primary driver for blockchain games; the Play-to-Earn (P2E) narrative is poised for a comeback, especially in a rising market. Games with superior economic models are likely to see greater success. For sustainable long-term development, a stable and well-designed tokenomic model is essential.

We extend our gratitude to the over 20 investment institutions that participated in our research survey for their valuable insights and contributions to this article.

Note: In this article, "probability of success" and "odds" are used to assess investment value. "Probability of success" refers to the likelihood of an investment being profitable. "Odds" refers to the potential magnitude of returns if the investment is successful.

Original link: https://research.huobi.com/#/ArticleDetails?id=312